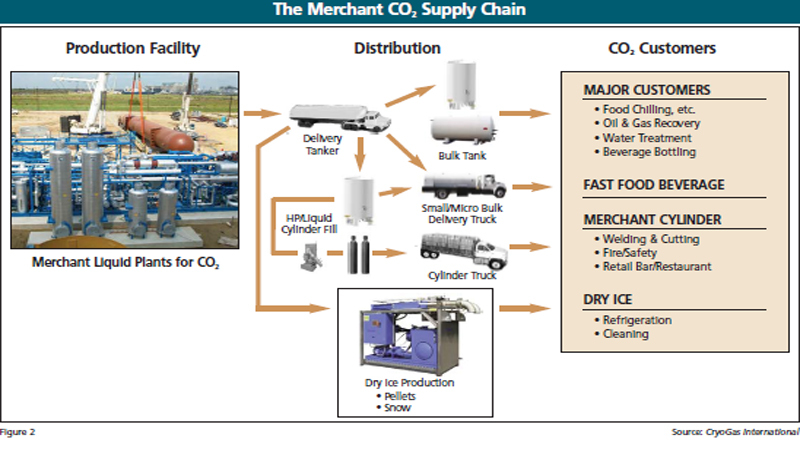

The carbon dioxide (CO2) industry is a complex one. Some companies within the industry both produce and distribute CO2, others buy crude and process it, while others are strictly distributors. The CO2 itself is delivered as crude, gas, liquid, and ice, and is sold as both pipeline and merchant, the latter of which includes bulk, microbulk, cylinder, and dry ice.

The merchant markets for carbon dioxide are varied, but food commandeers the largest piece of the pie. This segment includes carbonated beverage, food chilling and freezing, and dry ice used in food transport. The industrial sector represents the next largest share of the US CO2 market, where CO2 is used in metal working and in CO2 laser applications. Water treatment is another important application and growing market for carbon dioxide. In water treatment CO2 is used in recarbonation and pH control applications. Biofuels present a new market opportunity for CO2, as companies like Linde work on technologies that deliver CO2 to commercialscale, open-pond, algae-to-fuel cultivation systems. (See “Miniature Factories from the Sea,” November, 2011, p. 28.) In pipeline markets, CO2 is used for Enhanced Oil Recovery (EOR) in the fracking processes. (See “Unleashing the Economic Value of Unconventional Reservoirs Using Energized Fracturing” on p. 34.) This application is fast growing. In this report, we look at the supply chain and markets for CO2 in all its forms and how they performed in 2011.

Sourcing Carbon Dioxide

Government mandates on gas emissions, subsidies for clean fuels, and the price and availability of natural gas continue to impact the levels of capturing and sourcing CO2 across the spectrum in the US. As shown in Figure 1, the majority of crude CO2 (33 percent) is sourced from ethanol plants. While ethanol is being challenged by the surge in biofuel refineries and by the elimination of the federal tax credit for ethanol, its use continues to be mandated by governments as an additive to gasoline for environmental reasons. Those mandates are expanding so it is unlikely that sourcing CO2 from this process will diminish soon.

Hydrogen refining is also on the upswing as hydrogen demand in the oil refining industry continues to grow. (See “New Fuels, New Markets, Push Hydrogen Demand,” Cryo- Gas, April 2012, p. 26.) While still lagging ethanol production as a source of CO2 supply, the gap between the two has shrunk; hydrogen now has a 23 percent share, up one percent from 2010, while ethanol has a 33 percent share, down two percent.

... to continue reading you must be subscribed