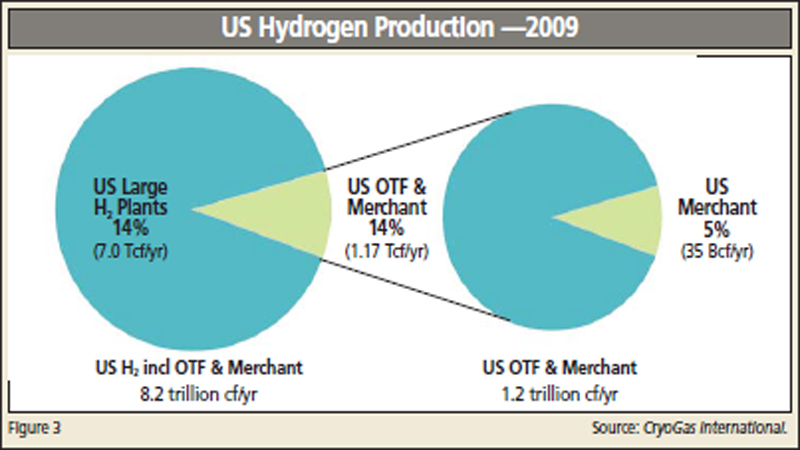

The hydrogen market is defined by two distinct segments: the large scale Onsite/ Pipeline (OSP) market and Merchant market. Each segment has unique market drivers and economics of hydrogen supply. The OSP market supplies large quantities of hydrogen to segments such as refining, basic and specialty chemicals, and food (starch). The Merchant market serves the small- to medium-hydrogen consumption requirement segments via bulk and cylinder.

Those segments include electronics, float glass manufacturing, hydrogenation of fat and oils for food, chemicals, cosmetic and pharmaceutical applications, heat treatment, the NASA space program, and alternative energy and research markets. In 2009, hydrogen sales to both OSP and Merchant markets were influenced by the worldwide recession. Some sectors, like refinery hydrogen and food, that continued to grow in developing markets and are fairly recession resistant, were able to take small steps forward, but others, like electronics and heat treatment, moved into weaker positions as demand in those sectors dropped dramatically.

Most hydrogen is produced from the process of steam methane reforming (SMR) of natural gas, on-site and by the largest users of hydrogen — refineries, fossil fuel processors, and ammonia producers. At oil refineries and integrated petrochemical sites the hydrogen used often comes as a by-product from other processes. The refining of heavier, sourer crudes requires more hydrogen than often is available from by-product sourcing. When this source is insufficient, dedicated hydrogen production is needed, and this is called “on-purpose” hydrogen production. The sharp increase in dedicated, on-purpose, hydrogen capacity that we have witnessed in the past ten years is driven by tighter global fuel specifications and the increased processing of heavier and sourer crudes.

... to continue reading you must be subscribed